The CARES Act Passed, What Do I Do Now?

April 3, 2020

The following information explains how the federal stimulus bill, known as the CARES Act, will provide assistance to workers, employers and others struggling financially during the COVID-19 pandemic.

Small Businesses

There are three primary financial helps for small businesses in the CARES ACT: (1) The Paycheck Protection Program, (2) Economic Injury Disaster Loans and (3) Business tax changes. These programs can be used separately or in connection with each other.

The Paycheck Protection Program sets aside $350 billion in government-backed loans from private banks that can, in some cases, be converted to grants, which means that you do not need to pay the loan back.

Paycheck Protection loans will come from 800 private lenders and are guaranteed by the SBA. The basic purpose is to incentivize small businesses to not lay off workers and to rehire laid-off workers that lost jobs due to COVID-19 disruptions. Loans are for small businesses with fewer than 500 employees, select types of businesses with fewer than 1,500 employees, 501(c)(3) non-profits with fewer than 500 workers, some 501(c)(19) veteran organizations, the self-employed, sole proprietors, and freelance and gig economy workers.

The maximum loan amount under the Paycheck Protection Act is $10 million, with an interest rate no higher than 4%. No personal guarantee or collateral is required for the loan. The lenders are expected to defer fees, principal and interest for no less than six months and no more than one year.

Some changes were made to the program in June 2020 by the Paycheck Protection Plan Flexibility Act.

Where can I apply for the Paycheck Protection Program?

You can apply for the Paycheck Protection Program (PPP) at any lending institution that is approved to participate in the program through the existing U.S. Small Business Administration (SBA) 7(a) lending program and additional lenders approved by the Department of Treasury. This could be the bank you already use, or a nearby bank. Here’s a list of participating CT lenders, look for the ones designated “GP.”

Who is eligible for the loan?

You are eligible for a loan if you are a small business that employs 500 employees or fewer, or if your business is in an industry that has an employee-based size standard through SBA that is higher than 500 employees. In addition, if you are a restaurant, hotel, or a business that falls within the North American Industry Classification System (NAICS) code 72, “Accommodation and Food Services,” and each of your locations has 500 employees or fewer, you are eligible. Tribal businesses, 501(c)(19) veteran organizations, and 501(c)(3) nonprofits, including religious organizations, will be eligible for the program. Nonprofit organizations are subject to SBA’s affiliation standards. Independently owned franchises with under 500 employees, who are approved by SBA, are also eligible. Eligible franchises can be found through SBA’s Franchise Directory.

I am an independent contractor or gig economy worker, am I eligible?

Yes. Sole proprietors, independent contractors, gig economy workers, and self-employed individuals are all eligible for the Paycheck Protection Program.

What is the maximum amount I can borrow?

The amount any small business is eligible to borrow is 250 percent of their average monthly payroll expenses, up to a total of $10 million. Loan amounts are calculated to cover 8 weeks of payroll expenses and any additional amounts for making payments towards debt obligations. Borrowers have 24 weeks to spend loan funds between February 15, 2020 and December 31, 2020. The loan must be fully expended by December 31, 2020. (updated by the Paycheck Protection Plan Flexibility Act in June, 2020)

How can I use the money such that the loan will be forgiven?

The amount of principal that may be forgiven is equal to the sum of expenses for payroll, and existing interest payments on mortgages, rent payments, leases, and utility service agreements. Payroll costs include employee salaries, hourly wages and cash tips, paid sick or medical leave, and group health insurance premiums. If you would like to use the Paycheck Protection Program for other business-related expenses, like inventory, you can, but that portion of the loan will not be forgiven. NOTE: Employees making more than $100,000 not eligible to be counted.

When is the loan forgiven?

The loan is forgiven at the end of the 24 week period (updated by the Paycheck Protection Plan Flexibility Act in June, 2020). Borrowers will work with lenders to verify covered expenses and the proper amount of forgiveness. Consult your lender for additional guidance.

What is the covered period of the loan?

The covered period during which expenses can be forgiven extends from February 15, 2020 to December 31, 2020 (updated by the Paycheck Protection Plan Flexibility Act in June, 2020).

How much of my loan will be forgiven?

The purpose of the Paycheck Protection Program is to help you retain your employees, at their current base pay. If you keep all your employees, the entirety of the loan will be forgiven. If you still lay off employees, the forgiveness will be reduced by the percent decrease in the number of employees. If your total payroll expenses on workers making less than $100,000 annually decreases by more than 25 percent, loan forgiveness will be reduced by the same amount. NOTE: If you have already laid off some employees, you can still be forgiven for the full amount of your payroll cost if you rehire your employees by December 31, 2020 (updated by the Paycheck Protection Plan Flexibility Act in June, 2020).

Am I responsible for interest on the forgiven loan amount?

No, if the full principal of the PPP loan is forgiven, the borrower is not responsible for the interest accrued in the 8-week covered period. The remainder of the loan that is not forgiven will operate according to the loan terms agreed upon by you and the lender.

What are the interest rate and terms for the loan amount that is not forgiven?

The terms of the loan not forgiven may differ on a case-by-case basis. The SBA issued a press release on March 31, 2020 announcing that all loans under this program will have the following identical features:

• Interest rate of 0.5%

• Maturity of 5 years (updated by the Paycheck Protection Plan Flexibility Act in June, 2020)

• First payment deferred for six months

• 100% guarantee by SBA

• No collateral

• No personal guarantees

• No borrower or lender fees payable to SBA

You will not have to pay any fees on the loan. Collateral requirements and personal guarantees are waived. Loan payments will be deferred for at least six months and up to one year starting at the origination of the loan.

When is the application deadline for the Paycheck Protection Program?

Applicants are eligible to apply for the PPP loan until June 30th, 2020.

I took out a bridge loan through DECD, am I eligible to apply for the Paycheck Protection Program?

Yes, you can take out a state bridge loan and are still be eligible for the PPP loan.

If I have applied for, or received an Economic Injury Disaster Loan (EIDL) related to COVID- 19 before the Paycheck Protection Program became available, will I be able to refinance into a PPP loan?

Yes. If you received an EIDL loan related to COVID-19 between January 31, 2020 and the date at which the PPP becomes available, you would be able to refinance the EIDL into the PPP for loan forgiveness purposes. However, you may not take out an EIDL and a PPP for the same purposes. Remaining portions of the EIDL, for purposes other than those laid out in loan forgiveness terms for a PPP loan, would remain a loan. If you took advantage of an emergency EIDL grant award of up to $10,000, that amount would be subtracted from the amount forgiven under PPP.

What does Payroll include?

The CARES Act states that payroll includes:

Salary, wage or similar compensation; Payment of cash tips or equivalent; Payment for vacation, parental, family, medical, or sick leave; Allowance for dismissal or separation; Payment required for the provisions of group health care benefits, including insurance premiums; Payment of any retirement benefit; Payment of State or local tax assessed on the compensation of employees; plus The sum of payments of any compensation to or income of a sole proprietor or independent contractor that is a wage, commission, income, net earnings from self-employment, or similar compensation and that is in an amount that is not more than $100,000 in 1 year, as prorated for the covered period;

It does not include: The compensation of an individual employee in excess of an annual salary of $100,000, as prorated for the covered period; Certain taxes imposed or withheld during the time period; Any compensation of an employee whose principal place of residence is outside the United States; Qualified sick leave wages for which a credit is allowed under section 7001 of the Families First Coronavirus Response Act (Public Law 116–6 127); Qualified family leave wages for which a credit is allowed under section 7003 of the Families First Coronavirus Response Act (Public Law 116–12 127);

What Do Utilities Include?

Utilities include electricity, gas, water, transportation, telephone, or internet access for which service began before February 15, 2020.

Can I Apply for This Loan and the Payroll Tax Credit?

There is a payroll tax credit of up to 50% of qualified wages for certain businesses whose operations have been fully or partially suspended by a government order or whose gross receipts in a quarter have fallen by at least half compared to a similar quarter the year before. NOTE: Your business cannot receive both the Employee Retention Payroll Tax Credit and a Paycheck Protection Program Loan, so if you are considering both make sure you consult with your legal or financial advisor.

What Can I Do Right Now?

You can apply for the Paycheck Protection Program (PPP) at any lending institution that is approved to participate in the program through the existing U.S. Small Business Administration (SBA) 7(a) lending program and additional lenders approved by the Department of Treasury. This could be the bank you already use, or a nearby bank. Here’s a list of participating CT lenders, look for the ones designated “GP.” Banks are expected to start taking applications April 3, 2020. While you wait for these loans to become available there are several things you can do right now:

1. Gather payroll documentation. While we don’t have exact document requirements yet, you’ll need documents such as payroll tax filings verifying the number of full-time employees on payroll and how much they were paid during the applicable time period. (See “How Much Can I Borrow” above.) If necessary, contact your accountant, bookkeeper or payroll processing firm to make sure you have the documents you need. If you are self-employed, see “I Don’t Have Employees.”

2. Check your credit. It’s likely these loans will still require a credit check. Even if the SBA doesn’t require it. If you don’t know where you stand, it’s a good idea to check your personal and business credit. You can do that for free at Nav.com and we will also alert you when our lending partners begin to make these loans and help match you to lenders.

3. Get clear on your finances. If you have let your bookkeeping fall behind, catch up. You need a clear picture of your income and expenses to make decisions about how your business will weather the crisis. If you hope to apply for loan forgiveness, you’ll also need documentation of the expenses you will pay during the 8-weeks after you get the loan, including mortgage interest and/or rent and utilities.

Paycheck Protection Program Loans may prove to be a crucial tool helping some small businesses survive this crisis. Although this may seem overwhelming, it’s worth taking the time to find out how they may help your business.

The SBA’s disaster loan program was extended to all small businesses affected by COVID-19. CARES Act opens this program up further and makes it easier to apply. These loans come directly from the SBA and you can apply for one here.

These changes include:

EIDLs are now also available to Tribal businesses, cooperatives, and ESOPs with fewer than 500 employees. They are also available to all non-profit organizations, including 501(c)(6)s, and to individuals operating as sole proprietors or independent contractors.

EIDLs can be approved by the SBA based solely on an applicant’s credit score.

EIDLs that are smaller than $200,000 can be approved without a personal guarantee.

Borrowers can receive a $10,000 emergency grant cash advance that can be forgiven if spent on paid leave, maintaining payroll, increased costs due to supply chain disruption, mortgage or lease payments or repaying obligations that cannot be met due to revenue losses.

EIDL Loans Applications are done on-line at the SBA website.

The CARES Act makes select changes to taxes and tax policies in order to ease the burden on businesses impacted by COVID-19. These changes include:

An employee retention tax credit if 1) your business operations were fully or partially suspended due to a COVID-19 shut-down order; or 2) gross receipts declined by more than 50% compared to the same quarter in the prior year. Eligible businesses can get a refundable 50% tax credit on wages up to $10,000 per employee. The credit can be obtained on wages paid or incurred from March 13, 2020, through December 31, 2020.

Businesses and self-employed individuals can delay their payroll tax payments. These payments can be deferred and paid over the next two years. Fifty percent must be paid by the end of 2021 and 50% must be paid by the end of 2022. (The ability to defer these taxes does not apply to a business that has a Paycheck Protection loan forgiven.)

If your business had a Net Operating Loss in a tax year beginning in 2018, 2019, or 2020, that NOL can be now be carried back five years. Pass-through businesses and sole proprietors will also be able to take advantage of the relaxed NOL limitations.

Businesses that were due to receive corporate alternative minimum tax (AMT) credits at the end of 2021 can claim a refund now.

Businesses will be able to increase their business interest expense deductions on their tax returns. For 2019 and 2020, the amount of interest expense businesses are allowed to deduct on their tax returns is increased to 50% from 30% of taxable income.

Businesses will be able to immediately write off costs associated with improving facilities.

The government will make a temporary exception from the excise tax normally applied to alcohol, if that alcohol was used to produce hand sanitizer in 2020.

Many of these changes will apply to small businesses all over the country, so it is vital to discuss with a tax professional which can apply to your company.

I own my own business and have no employees, work has slowed down (or shut down completely) I have no income, do I qualify for unemployment?

Yes, under this new provision self-employed individuals (including gig workers and independent contractors) part-time employees, and individuals with limited work histories.

But I haven’t paid any Unemployment Insurance premiums into the Unemployment Insurance Trust Fund, do I still qualify for the benefits?

Yes, while the benefits are administered by the states, the unemployment benefit you are receiving is funded by the Federal government, not the state’s Unemployment Insurance Trust Fund.

Even though I am a one-person operation, are the SBA programs in the CARES ACT available to me?

Yes. You may be eligible for all of the same programs as larger Small Businesses, or unemployment. There are three primary financial helps for small businesses in the CARES ACT: (1) The Paycheck Protection Program, (2) Economic Injury Disaster Loans and (3) Business tax changes. These programs can be used separately or in connection with each other.

Employees & Individuals

I am employed but sick with COVID 19, can I take paid sick leave?

Yes, if you are an employee at a company with 500 or less employees, you can take paid sick leave under the Emergency Paid Sick Leave Act.

I am employed but a family member is sick with COVID 19, can I take paid sick leave?

Yes, if you are an employee at a company with 500 or less employees, you can take paid sick leave under the Emergency Paid Sick Leave Act. The act’s Public Health Emergency Leave is available when an employee cannot work or telework because his or her minor child’s child care provider, school, or place of care is unavailable due to a public health emergency (i.e., an emergency with respect to COVID-19 declared by a federal, state, or local authority). An employee who needs to take public health emergency leave must notify his or her employer as practicable.

I am employed but my child’s day care is closed, can I take paid sick leave?

Yes, if you are an employee at a company with 500 or less employees you can take paid sick leave under the Emergency Paid Sick Leave Act.

I am employed but someone at my office has COVID 19, can I take paid sick leave?

No, paid sick leave is only available to individuals caring for themselves or a family member with who is subject to a COVID-19 quarantine or isolation order or to care for a minor child who does not otherwise have care due to the minor child’s child care provider, school, or place of care is unavailable due to a public health emergency.

However, you can take paid sick leave if you have COVID-19 symptoms and are seeking a medical diagnosis or if you have been advised by a health care provider to self-quarantine due to concerns related to COVID-19.

I am employed but I am fearful of leaving my house due to contracting COVID-19, can I take paid sick leave?

No, paid sick leave is only available to individuals caring for themselves or a family member who is subject to a COVID-19 quarantine or isolation order or to care for a minor child who does not otherwise have care due to the minor child’s child care provider, school, or place of care is unavailable due to a public health emergency

I am employed but a family member has a compromised immune system and I am fearful of contracting COVID-19 and spreading it to that person, can I take paid sick leave?

No, paid sick leave is only available to individuals caring for themselves or a family member who is subject to a COVID-19 quarantine or isolation order or to care for a minor child who does not otherwise have care due to the minor child’s child care provider, school, or place of care is unavailable due to a public health emergency

I am unemployed and exhausted my UI benefits before this started, what can I do?

The CARES Act provides an additional 13 weeks of unemployment benefits to workers who need beyond the 26 weeks provided under Connecticut law. The Connecticut Department of Labor is still awaiting guidance on the parameters of eligibility from the U.S. Department of Labor.

I quit my job as the pandemic was starting because I was concerned for my health, what can I do?

In general, individuals who voluntarily leave employment are not eligible for unemployment benefits. However, there are limited reasons that you may still qualify including leaving work to care for a spouse, child or parent with an illness or disability, provided (1) you submitted medical documentation verifying the illness or disability and need for care and (2) your employer did not communicate an offer of leave, paid or unpaid, for the period of time needed to provide care.

I left my employer to take another job but my new employer postponed my start date, what can I do?

Yes, you are eligible for unemployment benefits under the recently passed federal CARES Act creating the Pandemic Unemployment Assistance program.

But I’ve been out of work since before the Governor’s expanded Executive Order that affected my business?

Benefits are retroactive to January 27, 2020.

How many weeks am I eligible to receive unemployment?

Connecticut provides 26 weeks of Unemployment Compensation. Including the additional 13 weeks, an individual is eligible for a total of 39 weeks of Unemployment Compensation.

I own my own business and have no employees, work has slowed down (or shut down completely) I have no income, do I qualify for unemployment?

Yes, under this new provision self-employed individuals (including gig workers and independent contractors) part-time employees, and individuals with limited work histories.

My work as slowed down dramatically and I am having trouble paying my bills, what can I do?

You can file for partial unemployment benefits under the Pandemic Unemployment Assistance program recently passed by the federal government.

I needed to stop working to care for my child because his or her day care closed, what can I do?

You can file for unemployment benefits under the Pandemic Unemployment Assistance program recently passed by the federal government.

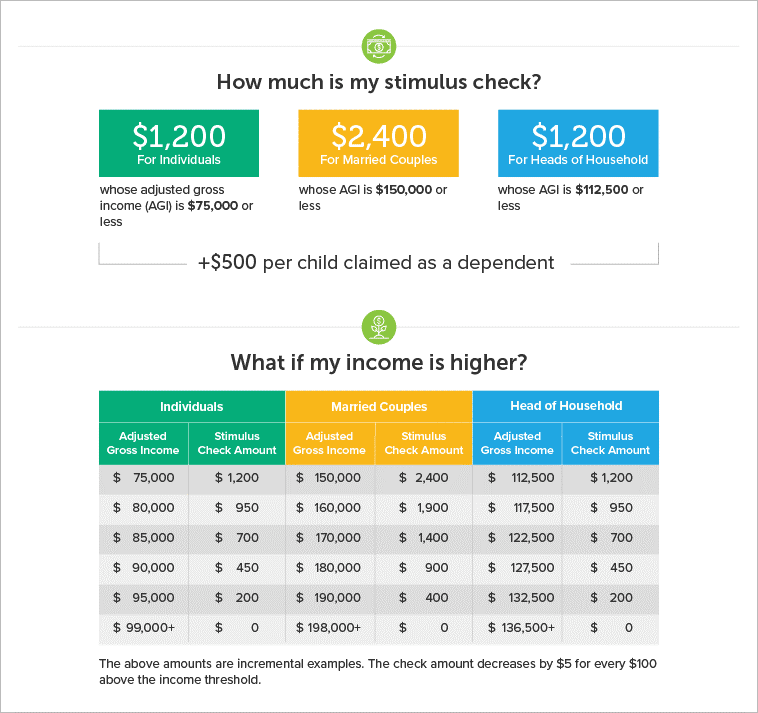

How much money will I receive from the Stimulus Payment?

It depends on your income. If you are a single adult, with an adjusted annual gross income of $75,000 or less, you can expect to receive the full amount of $1,200. Married couples with no children, who make $150,000 or less, would receive $2,400. If you are filing as a head of household and make $112,500 or less, this person would receive the full payment of $1,200. A family of four would receive $3,400. There would also be an additional payment of $500 for each child that is 16 or under. According to the IRS-issue number IR-2020-61, “For filers with income above those amounts, the payment amount is reduced by $5 for each $100 above the $75,000/$150,000 thresholds. Single filers with income exceeding $99,000 and $198,000 for joint filers with no children are not eligible.” (See chart below, courtesy of Reddit)

Has the IRS updated their website regarding direct payment information?

Yes, for specific guidance please review this website: https://www.irs.gov/newsroom/economic-impact-payments-what-you-need-to-know

Will there be more than one payment?

No-under this bill just the one.

When will I receive the payment?

Treasury Secretary Steven Mnuchin has stated that he is expecting more people to get their payments within three weeks (Week of April 17).

Do I have to sign up to receive my payments?

No.

Which year tax returns are being used to calculate how much money I will be receiving?

If you filed your 2019 returns, then tax year 2019 will be used. If you have not filed your 2019 return, then your 2018 return will be used.

What if I haven’t filed those tax returns?

According to the IRS issue number IR-2020-61, “the IRS urges anyone with a tax filing obligation who has not yet filed a tax return for 2018 or 2019 to file as soon as they can to receive an economic impact payment. Taxpayers should include direct deposit banking information on the return.”

How long will the payments last?

According to the IRS, “for those concerned about visiting a tax professional or local community organization in person to get help with a tax return, these economic impact payments will be available throughout the rest of 2020.”

How will I receive my check?

If IRS has your bank account info from previous filings for deposits to be made by direct deposit, it will be a direct deposit. If not, through the mail.

Are these payments taxable?

No.

Will the rebates affect my eligibility for federal income-targeted programs?

No, the rebate is considered a tax refund and is not counted towards eligibility for federal programs.

Social Security Recipients

Yes. Social Security beneficiaries who are not typically required to file tax returns will not need to file an abbreviated tax return to receive an Economic Impact Payment. Instead, payments will be automatically deposited into their bank accounts. The IRS will use the information on the Form SSA-1099 and Form RRB-1099 to generate $1,200 Economic Impact Payments to Social Security recipients who did not file tax returns in 2018 or 2019. Recipients will receive these payments as a direct deposit or by paper check, just as they would normally receive their benefits.

It depends on if your parents claim you as a dependent on their tax returns. If they do, you do not qualify.

Yes. The required minimum distribution from any IRAs or a 401(k) would not have to be taken in calendar year 2020.

You can also withdraw up to $100,000 this year and not have the 10% penalty. This must be regarding COVID-19 situation.

You can also still borrow from your 401(k) or other workplace retirements plans and can take out twice the usual amount. For 180 days after the bill passes, you can take out a loan of up to $100,000, if you have certification that you have been affected by the pandemic.

Landlords, Tenants and Homeowners

You should contact and work directly with your mortgage servicer to learn about and apply for available relief. Please note that financial institutions and their servicers are experiencing high volumes of inquiries.

You likely have a legal obligation pay your rent, but your landlord cannot evict you for 120 days. You should contact your landlord and see what you can work out. Under section 4024 of the Care Act, The Federal Government has placed a temporary moratorium on eviction filings if the property owner receives a federal subsidy or has a federally backed mortgage loan. The property owner may not file for eviction against or charge penalties or fees against a tenant who cannot pay rent for a period of 120 days after the enactment of the Care Act. This protection covers properties that receive federal subsidies such as public housing, Section 8 assistance, USDA rural housing programs, and Low-Income Housing Tax Credits, as well as properties that have a mortgage issued or guaranteed by a federal agency (including FHA and USDA) or Fannie Mae or Freddie Mac.

Homeowners with FHA, USDA, VA, or Section 184 or 184A mortgages and those with mortgages backed by Fannie Mae or Freddie Mac may request forbearance on their payments for up to 6 months, with a possible extension for another 6 months without fees, penalties, or extra interest. You should contact your mortgage provider to see if you qualify.

If your loan is with Fannie Mae mortgage relief options are available for homeowners who have been affected by COVID-19 is available on the Fannie Mae COVID-19 website.

On March 31, 2020, Connecticut announced a state mortgage relief agreement. Over 60 banks and credit unions have agreed to offer mortgage relief to homeowners and businesses facing hardship caused by the pandemic. These institutions may offer:

• A 90-day grace period for all mortgage payments;

• Relief from fees and charges for 90 days;

• No new foreclosures for 60 days; and

• No credit-score changes for accessing relief.

Contact your lender for more guidance on how this applies to your specific situation. More details and FAQs on this program available here.

How do I get mortgage relief and/or forbearance?

You should contact and work directly with your mortgage servicer to learn about and apply for available relief. Please note that financial institutions and their servicers are experiencing high volumes of inquiries.

How long will the forbearance last?

Participating financial institutions are now offering mortgage-payment forbearances of up to 90 days, which will allow homeowners to reduce or delay monthly mortgage payments.

What effect will this have on my credit report?

Financial institutions will not report derogatory information (e.g., late payments) to credit reporting agencies but may report a forbearance, which typically does not alone negatively affect a credit score.

How long will these programs last?

It is still unclear how severe or how long the COVID-19 impacts will be. Financial institutions have committed to necessary relief and will be assessing the ongoing conditions and necessity of continuing relief.

What if my financial institution isn’t offering this relief?

At this time, Webster Bank, American Eagle Financial Credit Union, Liberty Bank, Charter Oak Federal Credit Union, Bank of America, Nutmeg State Financial Credit Union, and Peoples United Bank, in addition to over 50 other federal and state-chartered banks, credit unions, and servicers are supporting these commitments. The state will welcome any other institution that would like to meet the moment and provide much-needed financial relief to Connecticut residents. The Department of Banking will publish a list of participating financial institutions on its website in the coming days.

What if I already made a payment or was hit with a fee because of COVID-19?

These measures go into effect as of March 31, 2020.

What if my mortgage servicer is not communicative or cooperative?

You can file a complaint with the Department of Banking through the complaint form on the department website or by contacting the department at 860-240-8299 or 1-800-831-7225 (9:00 am to 5:00 pm EST Monday through Friday).

The relief is currently only available for residential mortgages.