CARES Act Summary & FAQ

March 30, 2020

On March 27 the President signed into law the bipartisan Coronavirus Aid, Relief, and Economic Security (CARES) Act. The stimulus bill was designed to deliver urgently needed relief to our nation’s families, workers, and businesses and help our nation address the coronavirus pandemic.

Connecticut’s share of CARES Act funding is estimated to be $1.382 billion, of which $622 million is the maximum amount that can be allocate to municipalities with a population greater than 500,000.

Below is a summary of what is contained in the bill, followed by Frequently Asked Questions. The following contains information from the Office of U.S. Congressman Joe Courtney and the Office of U.S. Senator Chris Murphy. You can also view a Small Business Owner Guide to CARE Act from the U.S. Senate Committee on Small Business and Entrepreneurship here.

SUMMARY

The CARES Act contains the following major provisions:

- Checks of $1200 per adult, and $500 per child to American workers making less than $75,000 and under per year, to households making $150,000 per year and under. To obtain this federal funding, Americans need to have filed their taxes, or must file immediately.

- Expansion of Unemployment Insurance (UI), including extended benefits for 13 weeks, plus an extra $600 per week, and expanded eligibility for gig workers, self-employed Americans, and contractors.

- $367 billion in forgivable loans for small businesses who employ under 500 employees, for the purpose of helping to cover payroll, rent, and utilities. This resource is only for small businesses who keep their payrolls steady through the crisis. Small businesses who pledge to keep workers would also receive cash-flow assistance structured as federally guaranteed loans. If the employer continued to pay its workers for the duration of the crisis, those loans would be forgiven.

- $500 billion in Fed and Treasury lending to larger businesses, with guardrails including no stock buybacks, no increases in executive compensation, no money for businesses owned by the President’s family or for businesses owned by Members of Congress, 72-hour disclosure of all loans, subpoena power for the Inspector General, and an oversight board headed by the Inspector General and a 5-person panel appointed by Congress.

- $130 billion for hospitals to secure resources and training to prevent, treat, and respond to COVID-19, including critically needed Personal Protective Equipment (PPE)

- $150 billion in state, local, and tribal stabilization funds

- Roughly $200 billion in additional appropriations to meet additional needs

Frequently Asked Questions

Direct Payments

How will I know if I am getting a check or not? Do I have to sign up?

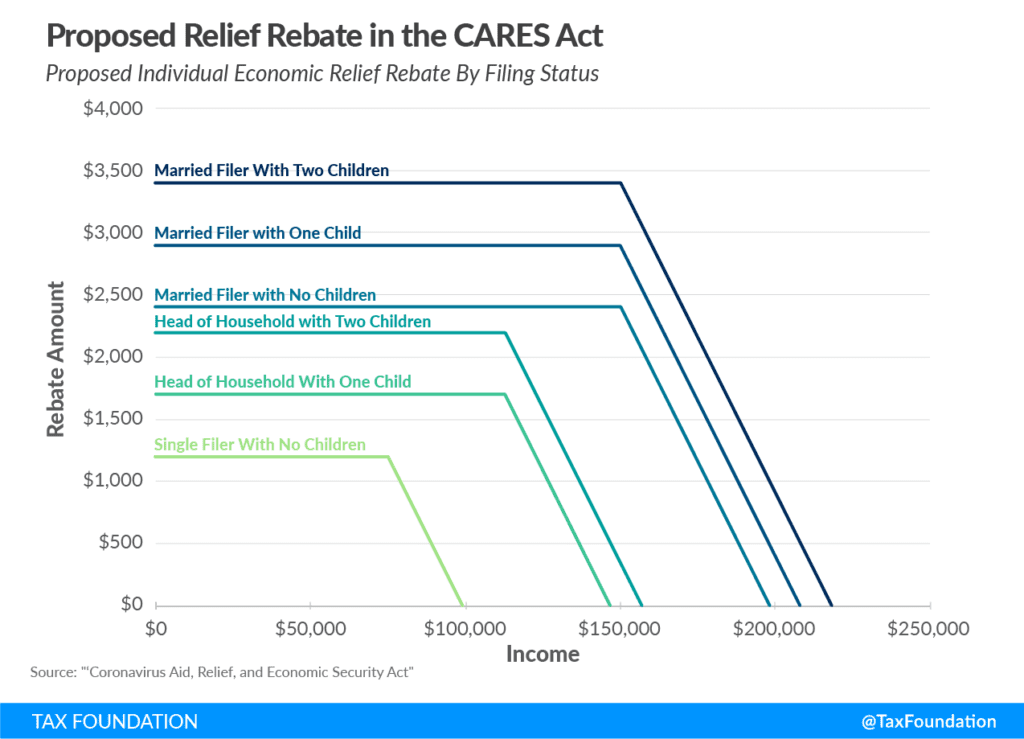

Individuals with adjusted gross income under $75,000 ($112,500 for head of household and $150,000 for joint filers) who are not dependents of another taxpayer are eligible for the full rebate.

The rebates will be paid out as advance refunds (in the form of checks or direct deposit) based on your 2019 tax returns (or 2018, if a 2019 return has not yet been filed).

Non-filers will have to file a tax return to qualify, but we are waiting on the IRS to provide more guidance.

These payments are available to anyone with a Social Security Number (but not an ITIN number), including those who have no income, as well as those whose income comes entirely from non-taxable, means-tested benefit programs, such as Social Security or Social Security Disability Insurance.

The rebate is treated like other refundable tax credits and not considered income, so it will not be taxed.

How much will I get and when?

Each eligible adult in a household will receive $1,200 with an additional $500 for each dependent child in the household under 17.

These payments begin phasing out at a 5% rate for single filers above $75,000, head of household filers above $122,500, and joint filers about $150,000. For example, an individual earning $87,000 per year would receive a payment of $600, and an individual earning $99,000 per year and above would not receive a payment.

If you make above those thresholds, the payment decreases, and it stops at single filers making $99,000 and married filers with no children at $198,000.

The IRS hopes to begin issuing the rebate checks within three weeks.

Will there be more than one payment?

No-under this bill just the one.

When will I receive the payment?

Treasury Secretary Steven Mnuchin has stated that he is expecting more people to get their payments within three weeks (Week of April 6).

Do I have to sign up to receive my payments?

No.

Which year tax returns are being used to calculate how much money I will be receiving?

If you filed your 2019 returns, then tax year 2019 will be used. If you have not filed your 2019 return, then your 2018 return will be used.

How will I receive my check?

If IRS has your bank account info from previous filings for deposits to be made by direct deposit, it will be a direct deposit. If not, through the mail.

I’m on social security. Will I still get a check?

Yes.

I’m a disabled vet, and I do not pay taxes. Will I receive a payment?

Yes.

What about college students. Do they qualify?

It depends on if your parents claim you as a dependent on their tax returns. If they do, you do not qualify.

Are these payments taxable?

No.

Unemployment Insurance (UI) and Emergency Leave

Am I eligible for UI?

You are eligible if you’ve been laid off, are working part-time, if you are self-employed, an independent contractor, and if you’re working in the “gig economy” because of COVID-19.

What is the benefit?

The exact amount you can receive through unemployment depends on your previous earnings and what you receive from the state, but between now and July 31, an additional $600 will be added to every unemployment compensation check, so no one will receive less than $600 per week. You can apply for unemployment insurance here.

If you exhaust the weeks of unemployment compensation available to you through CT DOL, you will be eligible for an additional 13 weeks of benefits. These benefits will be federally-funded, but you will still receive them through Connecticut.

The Families First Coronavirus Response Act provided $500 million for states to increase capacity to deal with unemployment insurance claims, which have been surging in Connecticut since early March.

Which employers must provide paid sick leave and family leave?

In general, a private employer with fewer than 500 employees is a “covered employer” for both the paid sick leave and paid family leave requirements.

The Secretary of Labor has additional authority to exempt employers with fewer than 50 employees from the requirement to provide leave for caring for children due to closures of schools or child care, both in the paid sick leave and paid family leave context.

How much paid sick leave are employees eligible to take?

For paid sick leave, employees are eligible to take up to 80 hours (two weeks) of paid time, depending on the employee’s regular schedule, at 100% of the employee’s regular rate of pay (up to $511 per day) due to quarantine/isolation order, health-care provider guidance to self-quarantine, or seeking diagnosis for symptoms of COVID-19.

Sick leave pay is limited to 2/3 of the employee’s regular rate of pay (up to $200 per day) for caring for someone who is isolated/quarantined and for taking care of a child due to a closure of school or child care.

How much paid family leave are employees eligible to take?

For paid family leave, employees are eligible to take up to 10 additional weeks of paid time at 2/3 of the employee’s regular rate of pay (up to $200 per day) solely to take care of a child due to a closure of school or child care or the unavailability of a child care provider.

Support for the State of Connecticut

What resources are provided for Connecticut to support critical efforts in the state to respond to this crisis?

The law includes $150 billion for a “Coronavirus Relief Fund” to send direct payments to states, tribal authorities, and local governments to help pay for necessary expenditures related to addressing the COVID-19 public health crisis. The state of Connecticut is expected to receive approximately $1.3 billion from this fund.

There’s also $1.5 billion to support state, local, and tribal public health department activities to be used for medical supplies, surveillance, lab testing, infection control and mitigation. Connecticut is estimated to receive almost $8 million from this fund to support state and municipal activities related to the COVID-19 response.

This is in addition to $950 million that Congress included in the first COVID-19 appropriations package. The Centers for Disease Control and Prevention provided $7.558 million on March 11 to Connecticut to support the state and local public health response.

Connecticut’s Health Care System

How can we make sure Connecticut is getting its share of money for medical supplies and Personal Protective Equipment for health care workers and first responders, as well as other?

The CARES Act includes $100 billion to ensure that health care providers continue to receive the support they need for COVID-19 related expenses and lost revenue that are otherwise unreimbursed. The HHS preparedness and response office plans to take applications on a rolling basis but has not yet opened up the process.

The CARES Act also includes $19.57 billion in funding to ensure the Department of Veterans Affairs (VA) has the equipment, tests, telehealth capabilities and support services necessary to support veterans and the health care workforce at facilities nationwide.

How do the laws support community health centers?

For community health centers on the front lines of testing and treating patients for COVID-19, the CARES Act provides $1.32 billion in new funding nationwide. The law also provides flexibility to expand telehealth coverage under Medicare to health centers.

The first COVID-19 appropriations bill provided $1.2 million in funding for 16 Federally Qualified Health Centers throughout Connecticut.

Will I have to pay for a coronavirus test?

The Families First Coronavirus Act waives cost-sharing (such as deductibles, coinsurance, or co-pays) for COVID-19 diagnostic testing and related health care services for individuals enrolled in private insurance plans, Medicare, Medicare Advantage, Husky/Medicaid, CHIP, TRICARE, VA as well as federal civilians, American Indians, and Alaska Natives. That law also prohibits plans from using tools like prior authorization to limit access to testing.

How does this law affect the cost of a vaccine when one becomes available?

The CARES Act ensures that once a vaccine is developed and is approved by the U.S. Government as a preventive measure that it will be covered by private insurers and free to Medicare beneficiaries with Part B.

This law also provides over $27 billion to support research and development of vaccines, therapeutics, and diagnostics to prevent or treat the effects of coronavirus.

These resources are in addition to $826 million to the National Institutes of Health to support basic research and the development of vaccines, therapeutics, and diagnostics; and $2 billion to support advanced research and development of vaccines, therapeutics, and diagnostics that was included in the first COVID-19 appropriations.

How does this law increase access to telehealth services for seniors and other Medicare Beneficiaries?

The Act allows more clinicians to provide telehealth services to Medicare beneficiaries, including in beneficiaries’ homes to avoid potential exposure to COVID-19, and provides more flexibility for health centers, rural health clinics, hospice physicians and nurse practitioners to utilize telehealth and remote patient monitoring services.

How can seniors and others get prescriptions filled while social distancing?

The law allows Medicare Part D recipients to get up to 90 days of a prescription, if that is what the doctor prescribed, as long as there are no safety concerns.

Medicare drug plans will also allow beneficiaries to fill prescriptions early for refills up to 90 days, depending on the prescription.

Governor Lamont also issued an Executive Order that provides pharmacists in the state with the discretion to fill a ninety-day refill of prescription drugs under certain circumstances.

Small Businesses

For a detailed small business owner’s guide please click here.

What relief is included for small businesses?

Paycheck Protection Program (PPP): The law includes nearly $350 billion to create a Paycheck Protection Program that will provide small businesses, nonprofits, and other entities with zero-fee loans of up to $10 million based on average monthly payroll costs. Up to eight weeks of average payroll, mortgage interest, rent, and utility payments can be forgiven if the business retains its employees and their salary levels. Principal and interest payments can be deferred for up to a year, and all SBA borrower fees are waived. This temporary emergency assistance through the U.S. Small Business Administration (SBA) and the Department of Treasury can be used in coordination with other COVID-financing assistance established in the law or any other existing SBA loan program.

Small Business Administration (SBA) Loans: The law also includes $17 billion to further ease the burden on small businesses that use SBA loan products. Under the law, the SBA will cover all loan payments for existing SBA borrowers, including principal, interest, and fees, for six months. The loan amount is based on average total monthly payments for payroll for the 12-week period beginning February 15, 2019, or at the election of the eligible recipient, March 1, 2019, and ending June 30, 2019.

Emergency Economic Injury Grants: The law includes $10 billion in funding for a provision to provide an advance of $10,000 to small businesses and nonprofits that apply for an SBA economic injury disaster loan (EIDL) within three days of applying for the loan. EIDLs are loans of up to $2 million that carry interest rates up to 3.75% for companies and up to 2.75% for nonprofits, as well as principal and interest deferment for up to 4 years. The loans may be used to pay for expenses that could have been met had the disaster not occurred, including payroll and other operating expenses.

The EIDL grant does not need to be repaid, even if the grantee is subsequently denied an EIDL, and may be used to provide paid sick leave to employees, maintaining payroll, meet increased production costs due to supply chain disruptions, or pay business obligations, including debts, rent and mortgage payments.

Refundable tax credits: IRS will be posting information soon on these credits on its website (www.irs.gov), including information on how to obtain advance payment of these credits.

Payroll taxes: The law defers payroll through the end of 2020. Deferred taxes will not become due until end of 2021 and end of 2022, with 50% of the liability being paid at each date.

Employee retention tax credit: available for struggling businesses that are not eligible or choose not to participate in the new SBA Paycheck Protection Program.

Is my small business eligible for relief?

Paycheck Protection Program (PPP): This relief is available for small businesses, 501(c)(3) nonprofits, 501(c)(19) veterans organizations, or Tribal businesses with not more than 500 employees who were in operation on February 15, 2020. It is also available to sole proprietorships, independent contractors, and eligible self-employed individuals.

Small Business Administration Loans: This relief will be available to existing SBA loan borrowers and new borrowers who take out an SBA loan within six months after the president signs the law. Each program has different requirements, go here for more details.

Emergency Economic Injury Grants: The grant is available to small businesses, private nonprofits, sole proprietors and independent contractors, tribal businesses, as well as cooperatives and employee-owned businesses. Eligible grant recipients must have been in operation on January 31, 2020.

Refundable tax credits: The law makes the credits available for private-sector employers that are required to offer coronavirus related paid leave to employees.

Payroll taxes: Any business that does not have a loan forgiven under the new SBA Paycheck Protection Program is eligible for the payroll tax deferral.

Employee retention tax credit: The law provides a refundable payroll tax credit for 50% of wages paid by employers to furloughed or reduced-hour employees during the COVID-19 crisis.

If I receive a stimulus check from the federal government, will it impact my ability to file for bankruptcy?

No. Under this law, stimulus checks from the federal government cannot be used to determine whether you are eligible for filing bankruptcy.

If you file for Chapter 13 bankruptcy, you will not have to turn your stimulus check over to your creditors. This new relief will be available for one-year.

What assistance is there for nonprofits?

Nonprofits are eligible for payroll taxes deferment (see above).

Nonprofits are eligible for the Paycheck Protection Program (see above).

The law also allows any mid-sized nonprofit (between 500 and 10,000 employees) to get access to quick, low cost, government guaranteed credit through their local lender or financial institution. The Treasury Department and Federal Reserve will have a degree of flexibility in designing the new program, but the expectation is for loan terms to last for no more than five years and to cover up to 100% of payroll over the previous 180 days, or 50% of revenues for the past year, for eligible organizations. Borrowers will also commit to rehiring their workforce back to pre-existing levels upon the end of the COVID-19 health emergency.

Utility and Nutrition Assistance

Is there utility assistance and am I eligible?

The law provides an additional $900 million for LIHEAP to help lower income households heat and cool their homes. You can check your eligibility here.

Connecticut has also ordered our utilities not to terminate service to customers during this crisis.

Is there nutrition assistance and am I eligible?

The law provides $15.5 billion in additional funding for the Supplemental Nutrition Assistance Program (SNAP). You can check your eligibility here.

The law also provides $450 million for The Emergency Food Assistance Program (TEFAP) to assist food banks across the country. You can look up local food banks here.

The law also expands food delivery service for seniors to ensure that seniors eligible for certain nutrition assistance programs can still receive that assistance if they are practicing social distancing.

Housing

What if I can’t pay my rent?

The law provides additional protections from eviction for all renters who live in properties that receive a federal subsidy, such as public housing, Section 8 rental assistance vouchers or subsidies, USDA rental housing assistance, or Low Income Housing Tax Credits. It also covers any renters in properties where the owner has a federally backed mortgage loan, which includes loans backed by the FHA, USDA, and Fannie Mae and Freddie Mac.

Owners of multifamily rental properties with federally-backed loans will be eligible to receive forbearance on those loans for 90 days, during which period they may not evict or charge late fees or other penalties to tenants for nonpayment of rent.

Owners of federally-subsidized properties or properties with a federally-backed mortgage loan may not evict or charge penalties or fees to a tenant who cannot pay rent for 120 days following this act.

What if I need assistance with my mortgage?

The CARES Act provides American homeowners with important protections to help keep them in their homes. Homeowners with FHA, USDA, VA or other federally-backed mortgages including those guaranteed by Fannie Mae and Freddie Mac may request forbearance on payments for up to 12 months with no fees, penalties, or extra interest.

The law also includes a 60 day moratorium on foreclosures and evictions of homeowners with FHA, USDA, VA, or 184/184A loans, or whose mortgages are backed by Fannie Mae and Freddie Mac.

Education

What funding is provided to K-12 schools?

The law provides $13.5 billion for local school districts to continue providing educational services to their students, including planning for and coordinating during long-term school closures and purchasing educational technology to support online learning.

Another $3 billion is available in flexible formula funding to allow Governors to address the needs of elementary and secondary schools and institutions of higher education.

Do I get relief from my student loans?

The CARES Act requires the Secretary of Education to defer loan payments, principal and interest, for 6 months through September 30, 2020 without penalty for the borrower for all federally held loans.

The law also suspends any involuntary collection for defaulted loans, such as wage garnishment, reduction of tax refunds, or Social Security benefits.

The law also includes a tax break for up to $5,250 for borrowers who are receiving assistance on student loan payments from their employers.

Is there additional funding for college students?

The law provides $14.25 billion for higher education emergency relief for colleges and universities to respond to coronavirus, including providing grants to students to cover their basic needs.

Public colleges are also eligible for flexible formula funding from the Governor.

Students who are currently participating in the Federal Work Study program can continue to receive work-study payments from their institution if they are unable to work due to workplace closures.

Relief also exists for students who must drop out of school due to COVID-19. Students will have the portion of their student loan taken out for the semester canceled. Students who received a Pell Grant or subsidized student loan will not have those types of financial aid counted toward their lifetime limits.

Children and Families

Is there additional assistance for childcare and who is eligible?

The law provides an additional $3.5 billion for the Child Care and Development Block Grant (CCDBG) to provide child care assistance to health care sector employees, emergency responders, sanitation workers, and other workers deemed essential during the response to the coronavirus. States can use funding to provide subsidies to essential workers, reimburse providers directly, open emergency child care centers, or keep providers from going out of business.

The law also includes $750 million for Head Start to meet emergency staffing needs.

CCDGB and Head Start funds will be distributed to the states, who will then pass them along through their own programs.

Is there assistance for social service organizations and who is eligible?

The law provides an additional $1 billion to the Community Services Block Grant to support a wide range of social services and emergency assistance for those who need it most. Funding goes directly to local community-based organizations (usually the area Community Action Programs), upon application.

The law provides an additional $5 billion for the Community Services Block Grant, which will be determined by formula.

Retirement Accounts

Are there any changes regarding my retirement account in this package?

Yes. The required minimum distribution from any IRAs or a 401(k) would not have to be taken in calendar year 2020.

You can also withdraw up to $100,000 this year and not have the 10% penalty. This must be regarding COVID-19 situation.

You can also still borrow from your 401(k) or other workplace retirements plans and can take out twice the usual amount. For 180 days after the bill passes, you can take out a loan of up to $100,000, if you have certification that you have been affected by the pandemic.

(Key Points from the Office of U.S. Congressman Joe Courtney. Frequently Asked Questions from multiple sources including the Office of U.S. Senator Chris Murphy)